New fees are in effect at the Massachusetts Registery of Deeds. You can look them up here.

Massachusetts Recording Fees Update

- By Trisha Solio

- Posted

New fees are in effect at the Massachusetts Registery of Deeds. You can look them up here.

The Department of Revenue (DOR) just released the final version of its Short-Term Rental Regulations.

Read the full regulations here

Realtors® can provide mandated insurance - This means that Realtors® who provide services online,

The new Massachusetts short term rentals law applies to property rentals of less than 31 days. It includes an occupancy tax, statewide registry, insurance requirements, and inspections. Any property rented out for less than 14 days in one year is [...]

If you own and live in your Boston property as a primary residence, you may qualify for the residential exemption. The residential exemption reduces your tax bill by excluding a portion of your residential property’s value from taxation. This year, the residential exemption saves qualified Boston homeowners up to $2,538.47 on their tax [...]

The Surrealtors are happy to announce that Colette Sanborn is the winner of the 2016 Surrealtors Refer Madness Sweepstakes! We are awarding Colette a trip for 2 to Maui, Jamaica, Amsterdam... or the destination of her choice (maximum value $2,500.00), for referring her cousin, the delightful Joanna [...]

Want to search for homes wherever you are? Download our powerful new mobile app.

You can see homes for sale right where you are, or search by location. Sort by price, filter by number of bedrooms and more, let your friends know about it by social media or email. And of course, contact Trisha directly so she can help you take the next step.

Here's a great Boston Globe story about the classic of Jamaica Plain and Dorchester housing stock, the triple decker.

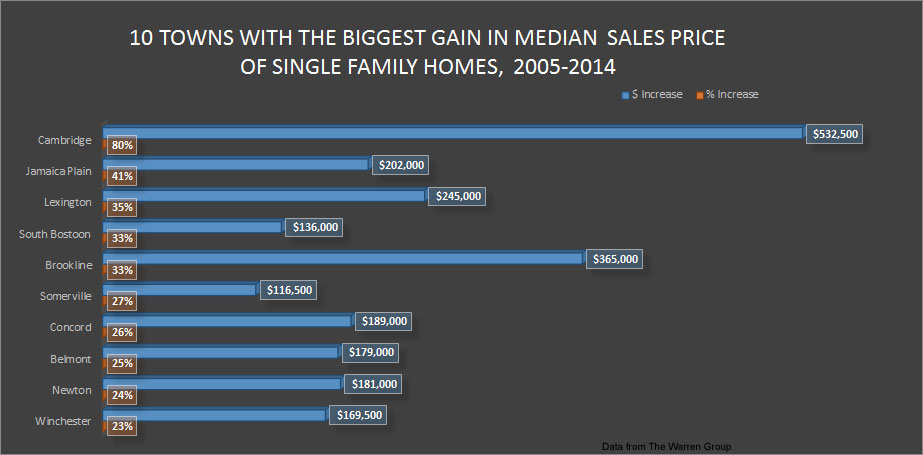

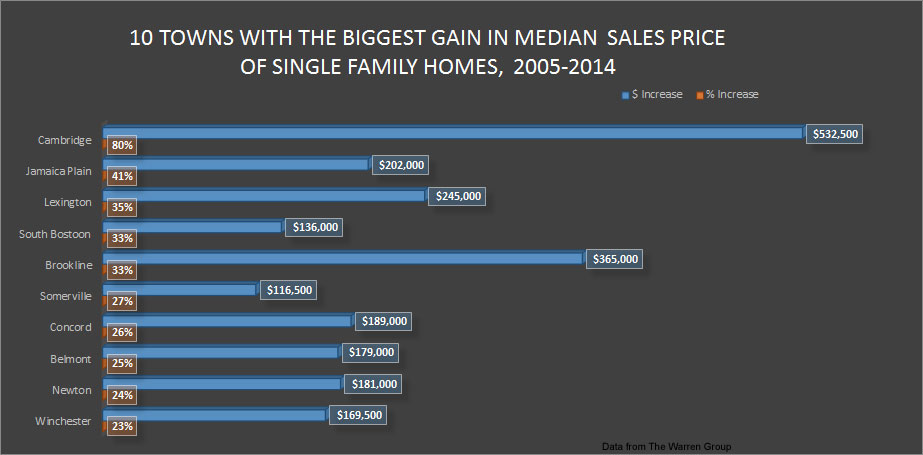

Home Values Increased in 10 Boston Area Towns and Neighborhoods

I have worked with many people through big life changes--buying a first home, selling that one and buying the next, sometimes numerous big moves.

Lately I've been getting a lot of calls to talk about the next phases of life. And I've been thinking about it myself.

In general, tax law identifies the difference between what a borrower owes and what a borrower actually pays to the bank in a foreclosure or short sale as taxable income. This can be a nightmare for already cash-strapped sellers. There is good news, [...]