Home Values Increased in 10 Boston Area Towns and Neighborhoods

Home Values Increased in 10 Boston Area Towns and Neighborhoods

I have worked with many people through big life changes--buying a first home, selling that one and buying the next, sometimes numerous big moves.

Lately I've been getting a lot of calls to talk about the next phases of life. And I've been thinking about it myself.

In general, tax law identifies the difference between what a borrower owes and what a borrower actually pays to the bank in a foreclosure or short sale as taxable income. This can be a nightmare for already cash-strapped sellers. There is good news, [...]

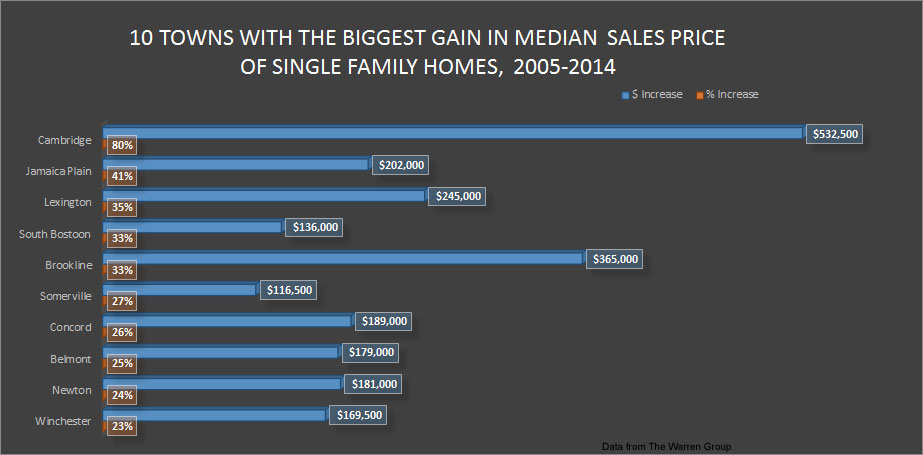

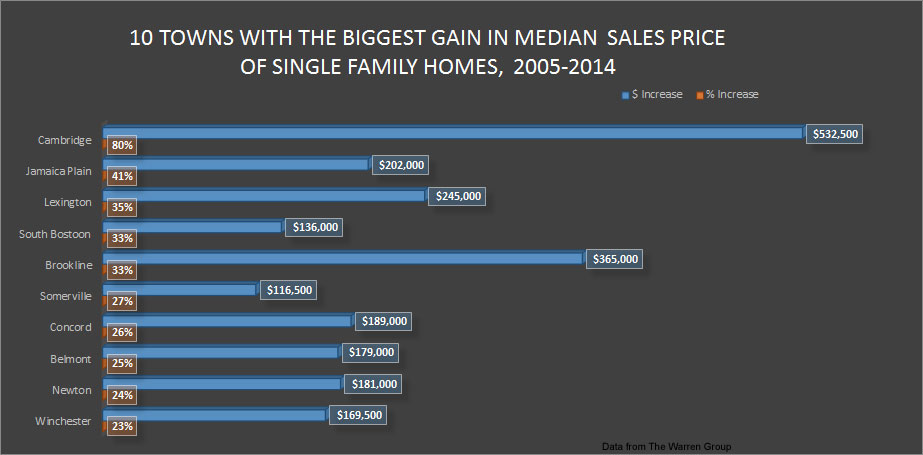

The Greater Boston Association of Realtors reports good news for home buyers in 2015.

For mortgages acquired by Fannie Mae and Freddie Mac, the conforming loan limit for a single-family home will remain at $417,000 next year for the majority of the country. In some markets, however, jumbo loan limits will rise, reflecting that these areas [...]